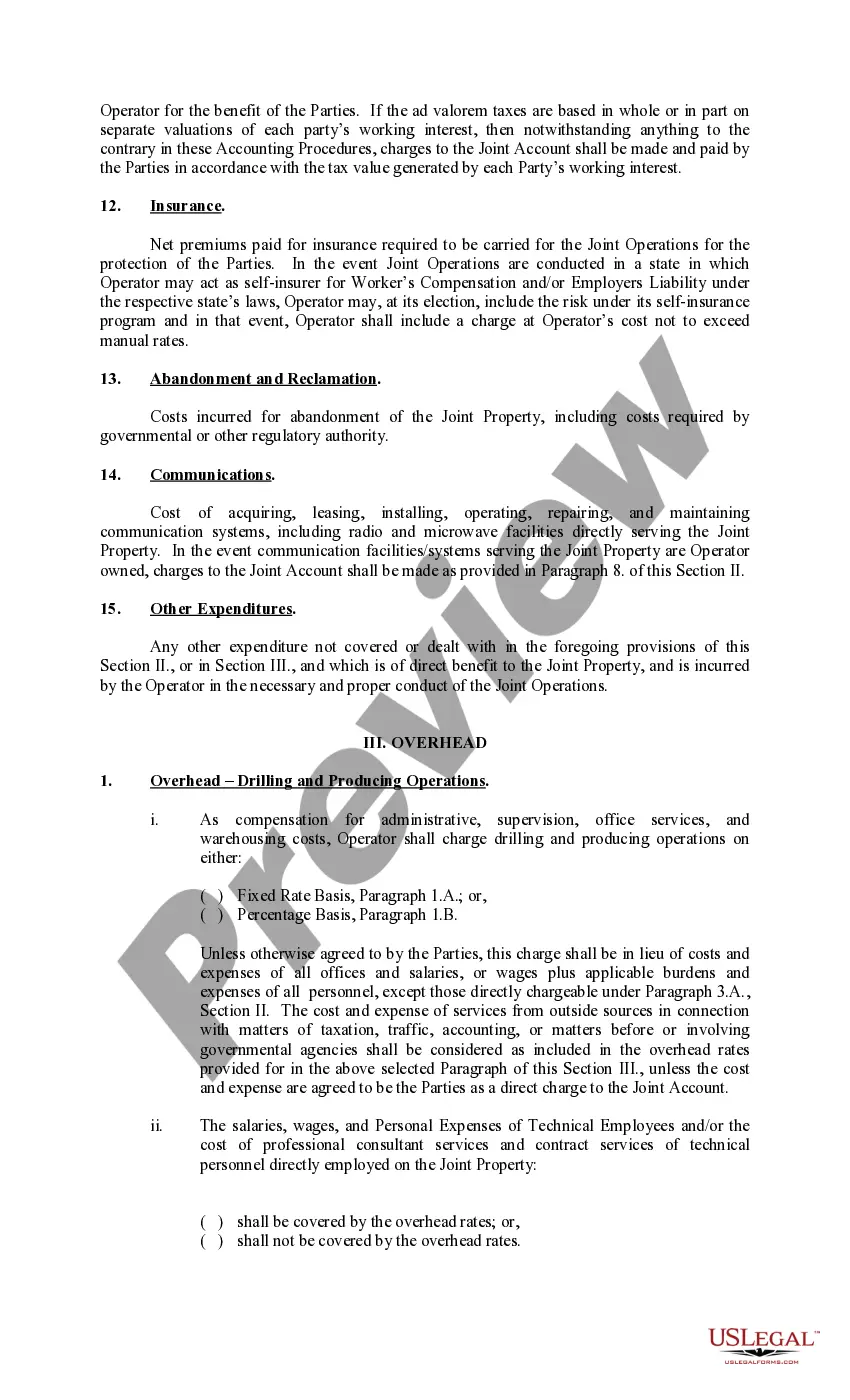

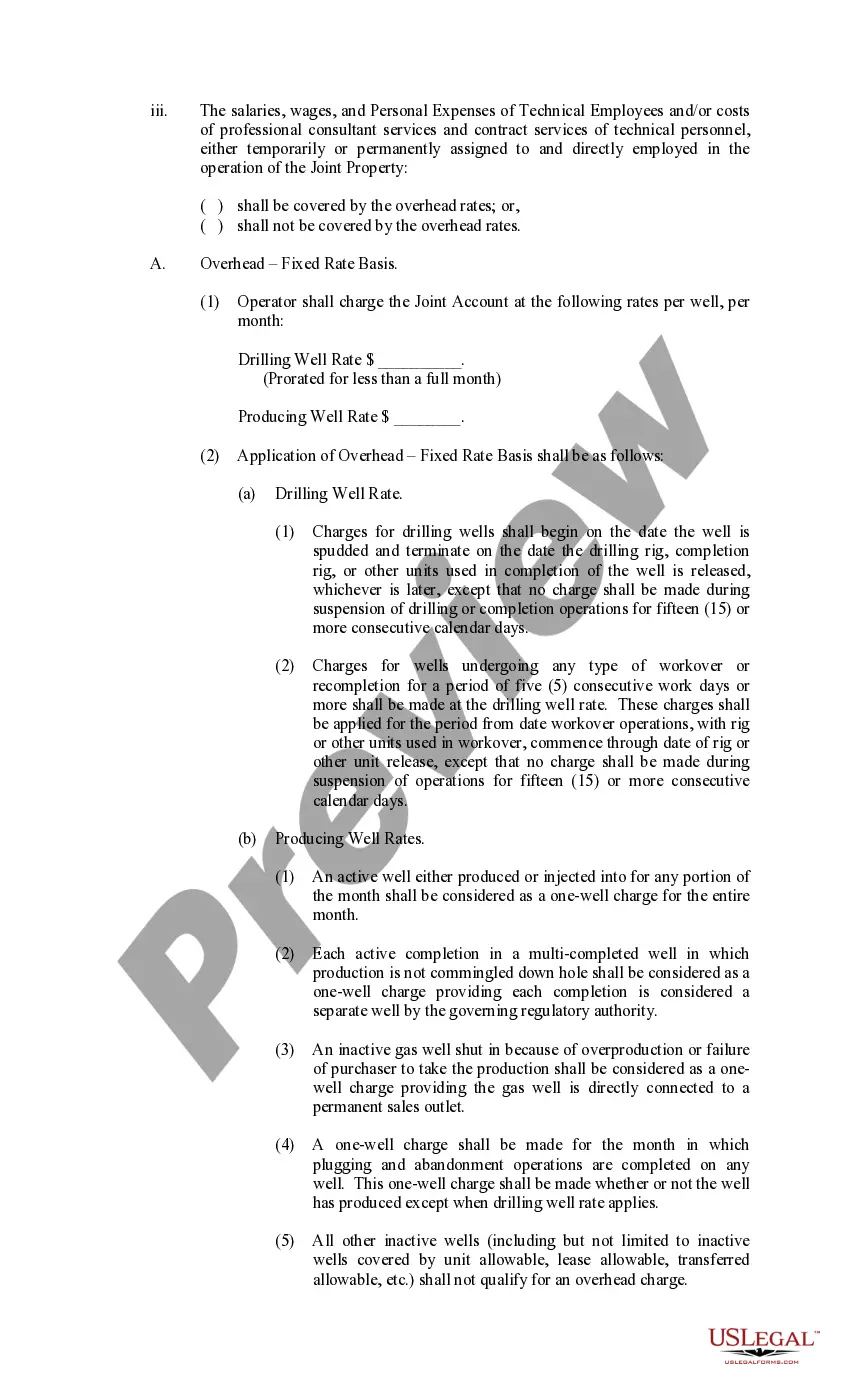

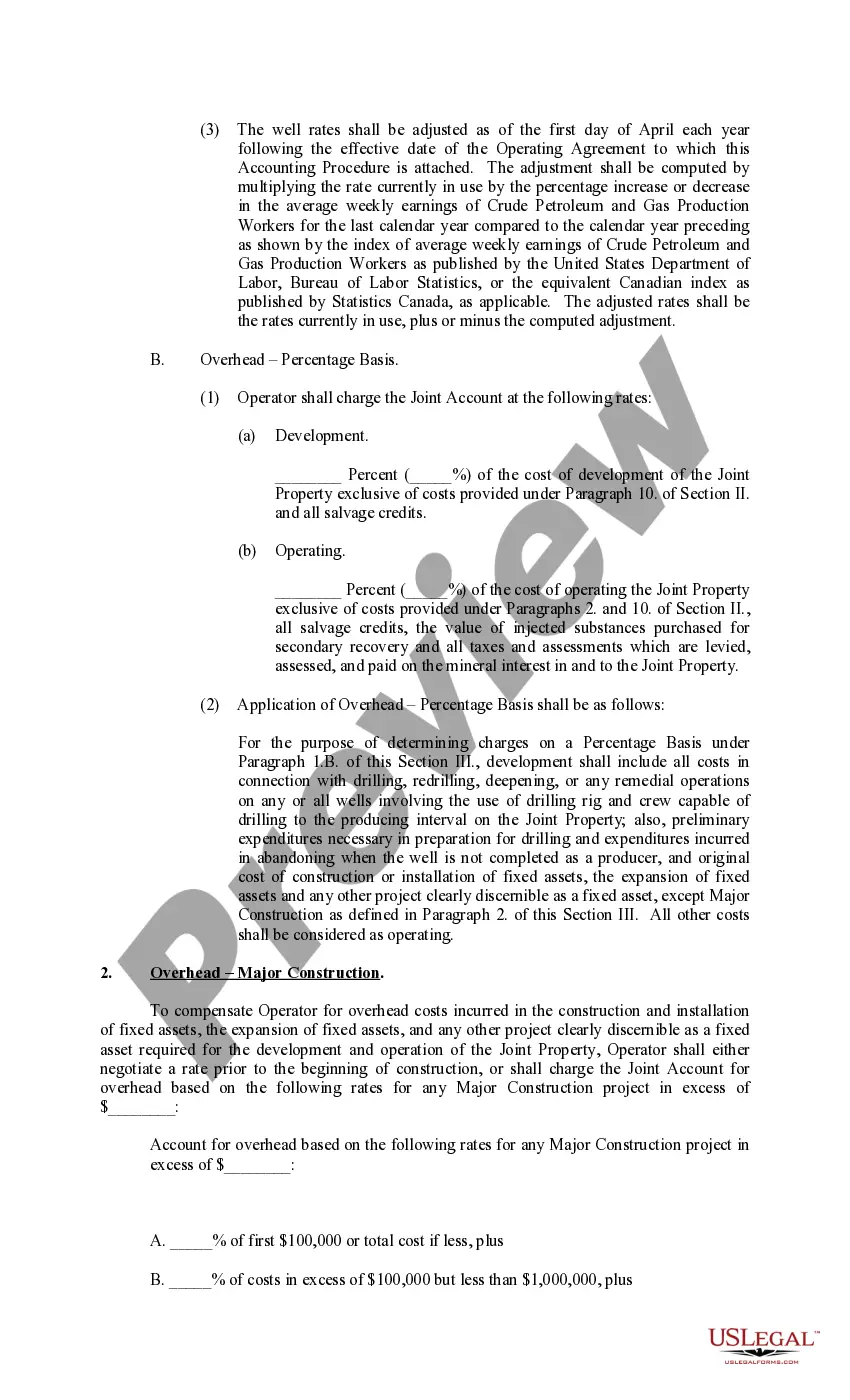

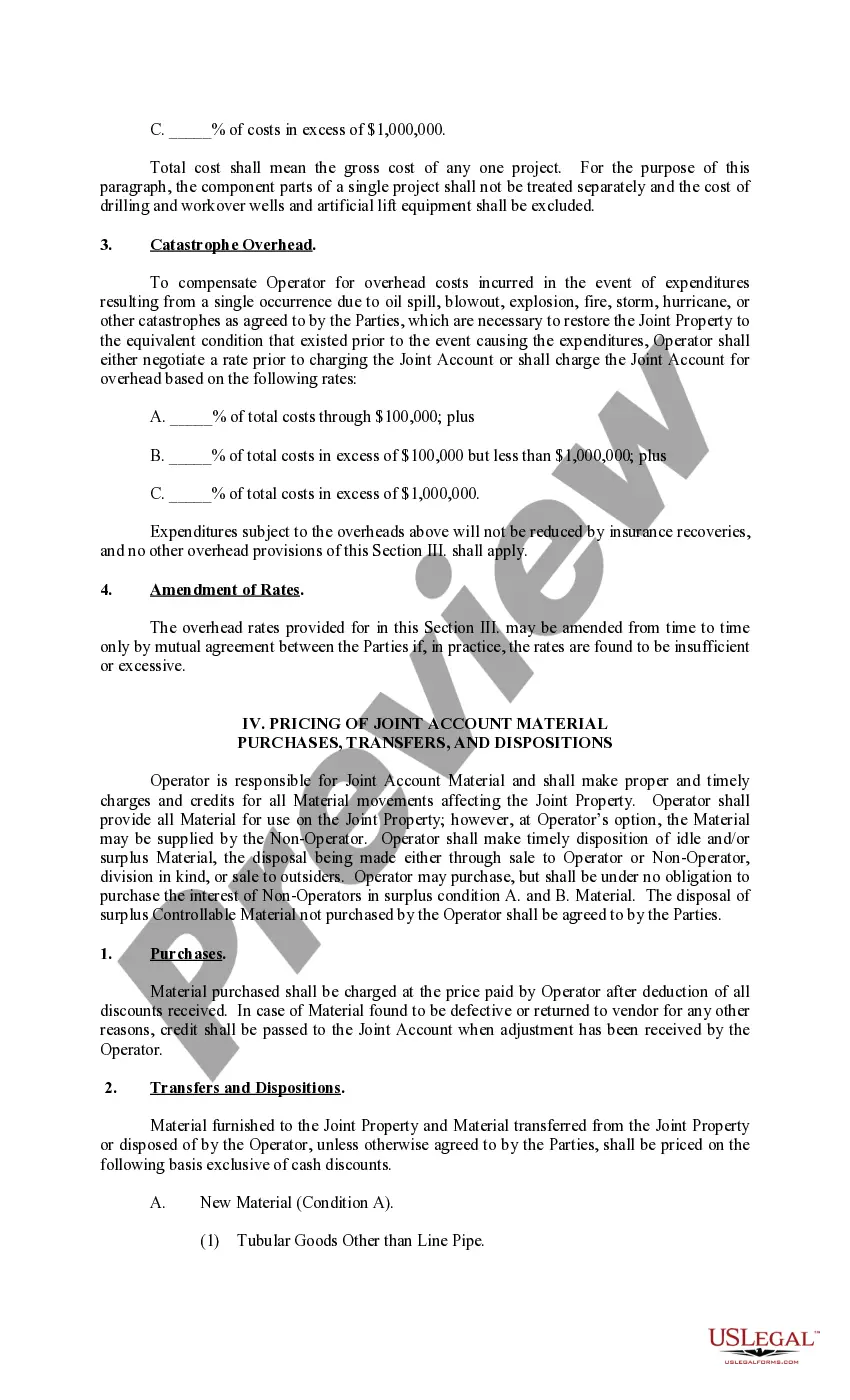

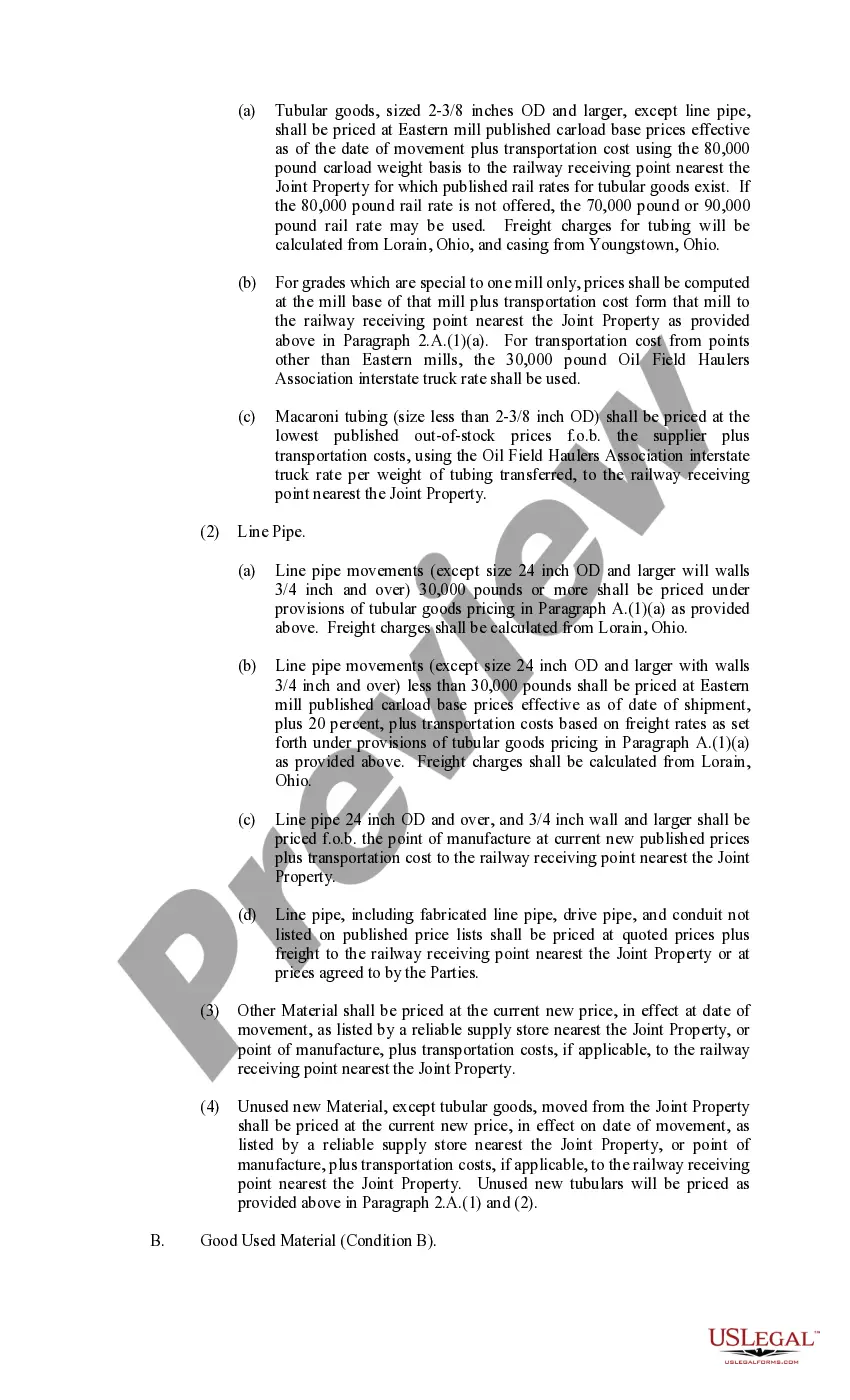

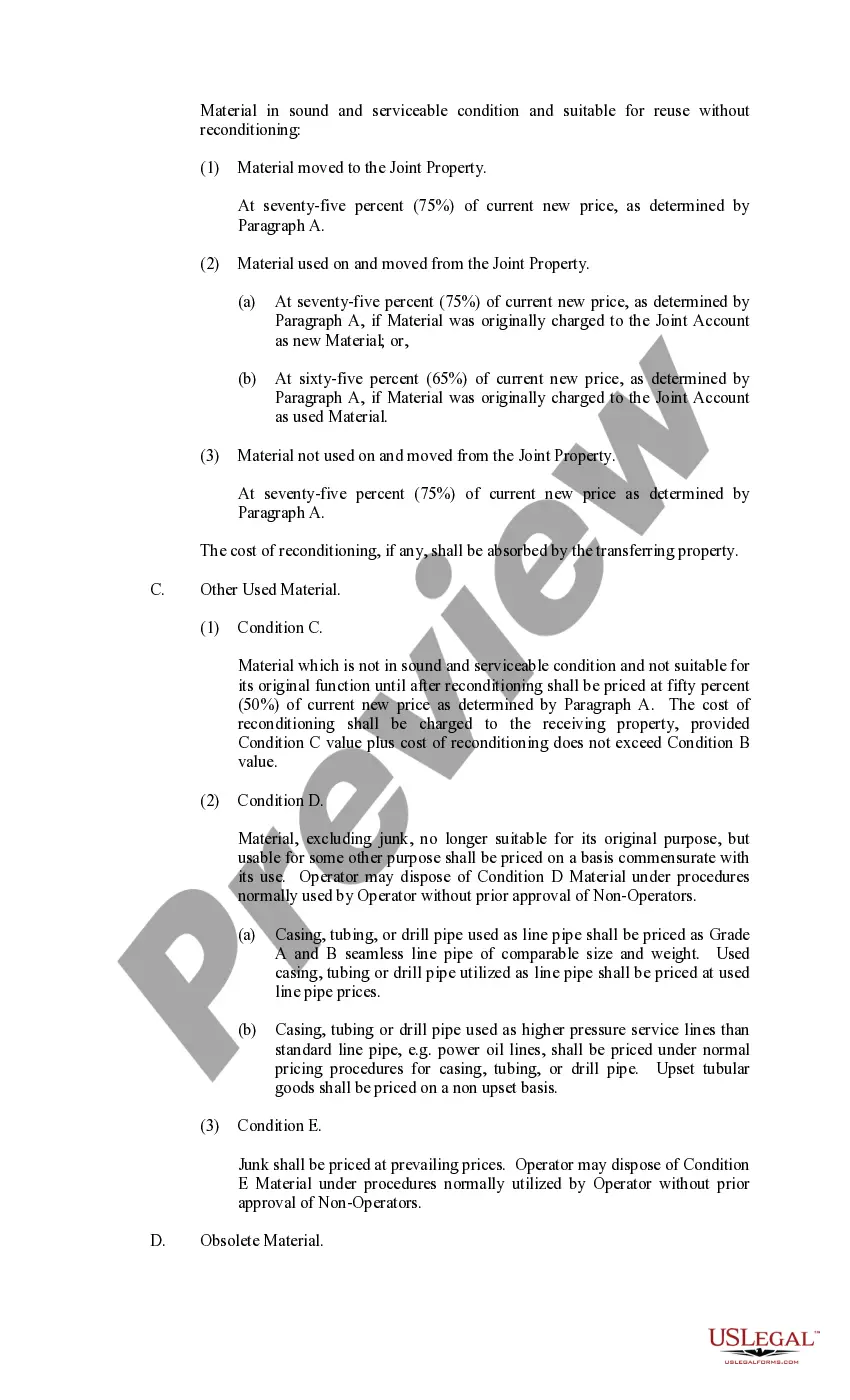

Suffolk New York Exhibit C Accounting Procedure Joint Operations is a comprehensive accounting process followed in joint operations conducted within Suffolk County, New York. This accounting procedure is specifically designed to ensure transparency, accuracy, and efficiency in financial management for joint operations. The primary objective of Suffolk New York Exhibit C Accounting Procedure Joint Operations is to establish a standardized framework for managing shared resources and expenses incurred during joint ventures, collaborations, or any other form of joint operations in Suffolk County, New York. By adhering to this procedure, accountability and financial control are maintained, ensuring fair distribution of costs and revenues among the participating parties. This accounting procedure covers various aspects that include recording, classifying, summarizing, and reporting financial transactions related to joint operations. Key elements of this procedure include: 1. Definition of Joint Operations: The procedure begins by defining the scope and nature of joint operations to ensure that all the involved parties have a clear understanding of their roles and responsibilities. 2. Cost Allocation: The procedure outlines a comprehensive method for allocating the costs incurred during joint operations, providing guidelines on how to determine shared expenses and to ensure fair distribution among the participating entities. 3. Revenue Recognition: The procedure includes guidelines for recognizing and distributing revenues generated from joint operations in Suffolk County, New York. It ensures that the revenue allocation is carried out fairly based on the agreed terms and conditions between the parties involved. 4. Reporting: Suffolk New York Exhibit C Accounting Procedure Joint Operations emphasizes regular and accurate reporting of financial information. It provides detailed instructions on preparing financial statements and reports, enabling transparency and facilitating informed decision-making for all parties. There can be different types of Suffolk New York Exhibit C Accounting Procedure Joint Operations, depending on the nature and purpose of the collaboration. Some examples include: 1. Joint Ventures: This type of joint operation entails two or more entities coming together to pursue a specific project or business opportunity in Suffolk County, New York. The accounting procedure outlines the financial management practices for such endeavors. 2. Public-Private Partnerships (PPP): This type of joint operation involves cooperation between public and private entities to deliver public services or infrastructural developments. The accounting procedure ensures proper financial management and accountability in such partnerships. 3. Consortium Projects: In the case of consortium projects, multiple organizations or agencies collaborate to achieve a common goal, such as research and development or community initiatives. Suffolk New York Exhibit C Accounting Procedure Joint Operations provides guidelines for financial management, ensuring smooth collaboration and equal cost-sharing. In summary, Suffolk New York Exhibit C Accounting Procedure Joint Operations is a crucial framework that governs financial management in joint endeavors within Suffolk County. With its comprehensive guidelines and instructions, this procedure promotes transparency, accuracy, and fair distribution of costs and revenues among the participating entities, ensuring successful joint operations in the county.

Suffolk New York Exhibit C Accounting Procedure Joint Operations

Description

How to fill out Suffolk New York Exhibit C Accounting Procedure Joint Operations?

Drafting paperwork for the business or personal needs is always a big responsibility. When drawing up an agreement, a public service request, or a power of attorney, it's essential to take into account all federal and state regulations of the particular region. However, small counties and even cities also have legislative procedures that you need to consider. All these aspects make it stressful and time-consuming to draft Suffolk Exhibit C Accounting Procedure Joint Operations without expert help.

It's possible to avoid wasting money on lawyers drafting your documentation and create a legally valid Suffolk Exhibit C Accounting Procedure Joint Operations by yourself, using the US Legal Forms web library. It is the greatest online collection of state-specific legal documents that are professionally verified, so you can be certain of their validity when choosing a sample for your county. Earlier subscribed users only need to log in to their accounts to save the needed form.

If you still don't have a subscription, follow the step-by-step guide below to get the Suffolk Exhibit C Accounting Procedure Joint Operations:

- Look through the page you've opened and verify if it has the sample you need.

- To accomplish this, use the form description and preview if these options are presented.

- To locate the one that suits your requirements, utilize the search tab in the page header.

- Recheck that the template complies with juridical standards and click Buy Now.

- Pick the subscription plan, then sign in or register for an account with the US Legal Forms.

- Utilize your credit card or PayPal account to pay for your subscription.

- Download the selected file in the preferred format, print it, or complete it electronically.

The exceptional thing about the US Legal Forms library is that all the documentation you've ever acquired never gets lost - you can get it in your profile within the My Forms tab at any time. Join the platform and quickly get verified legal forms for any use case with just a couple of clicks!