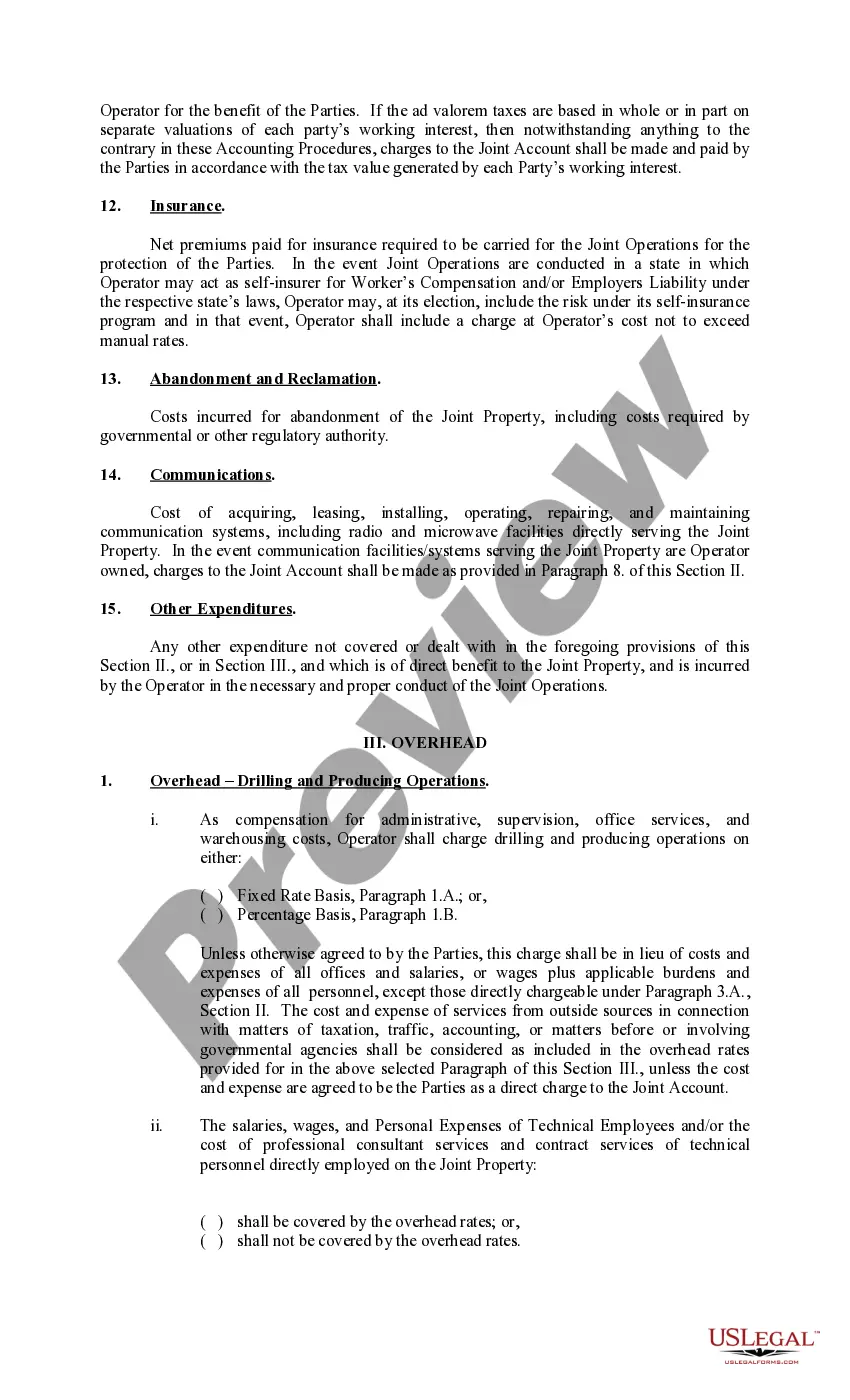

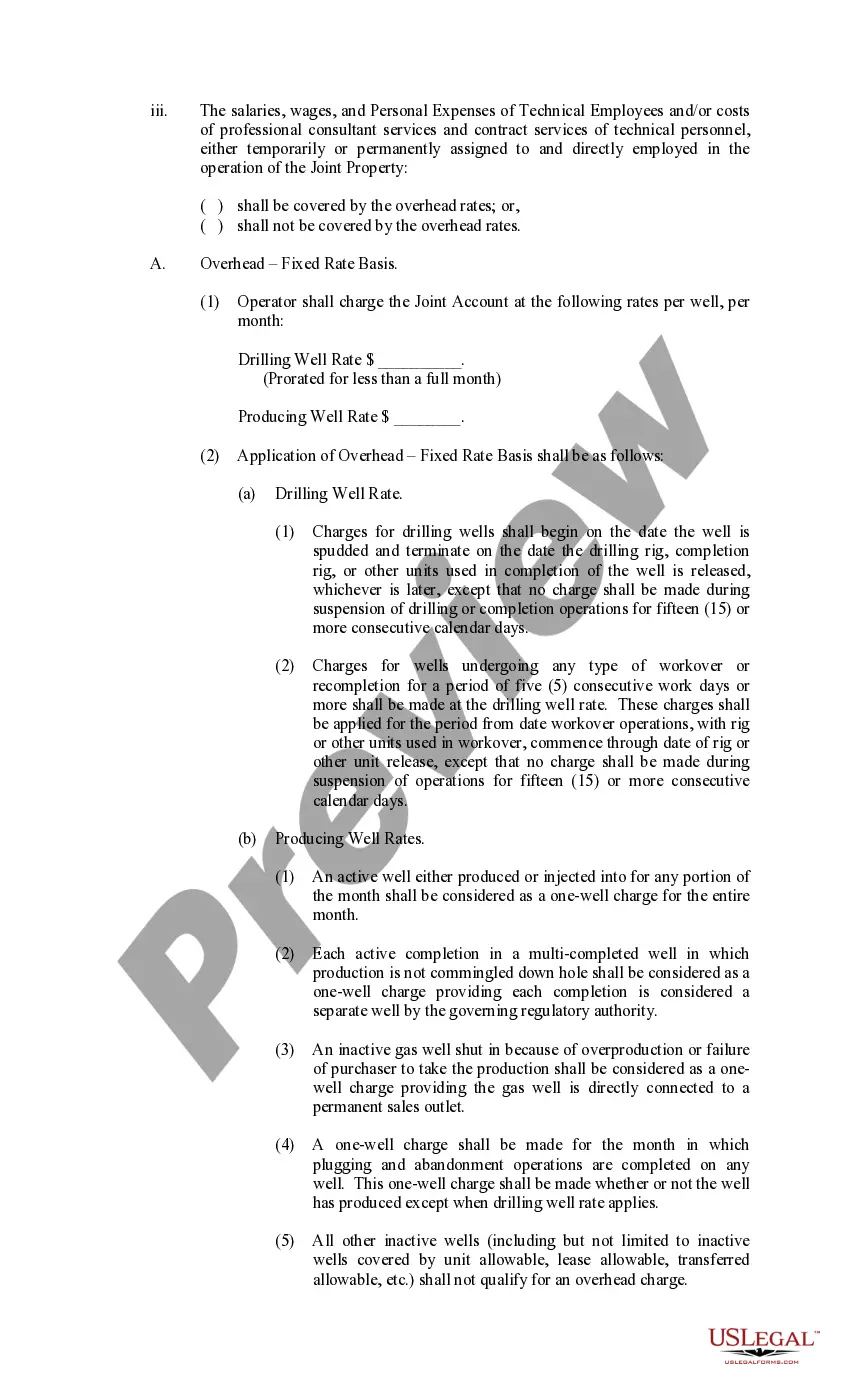

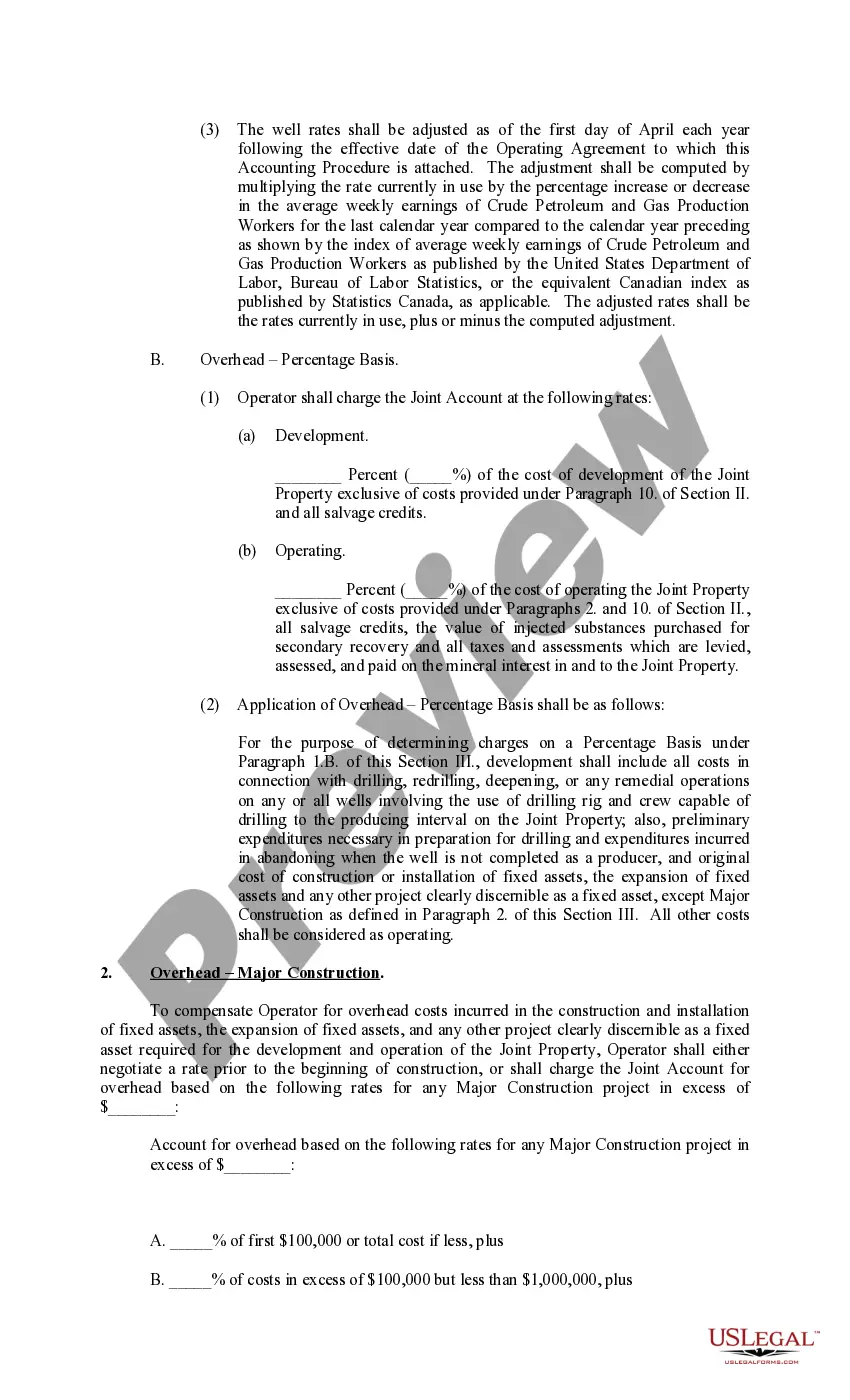

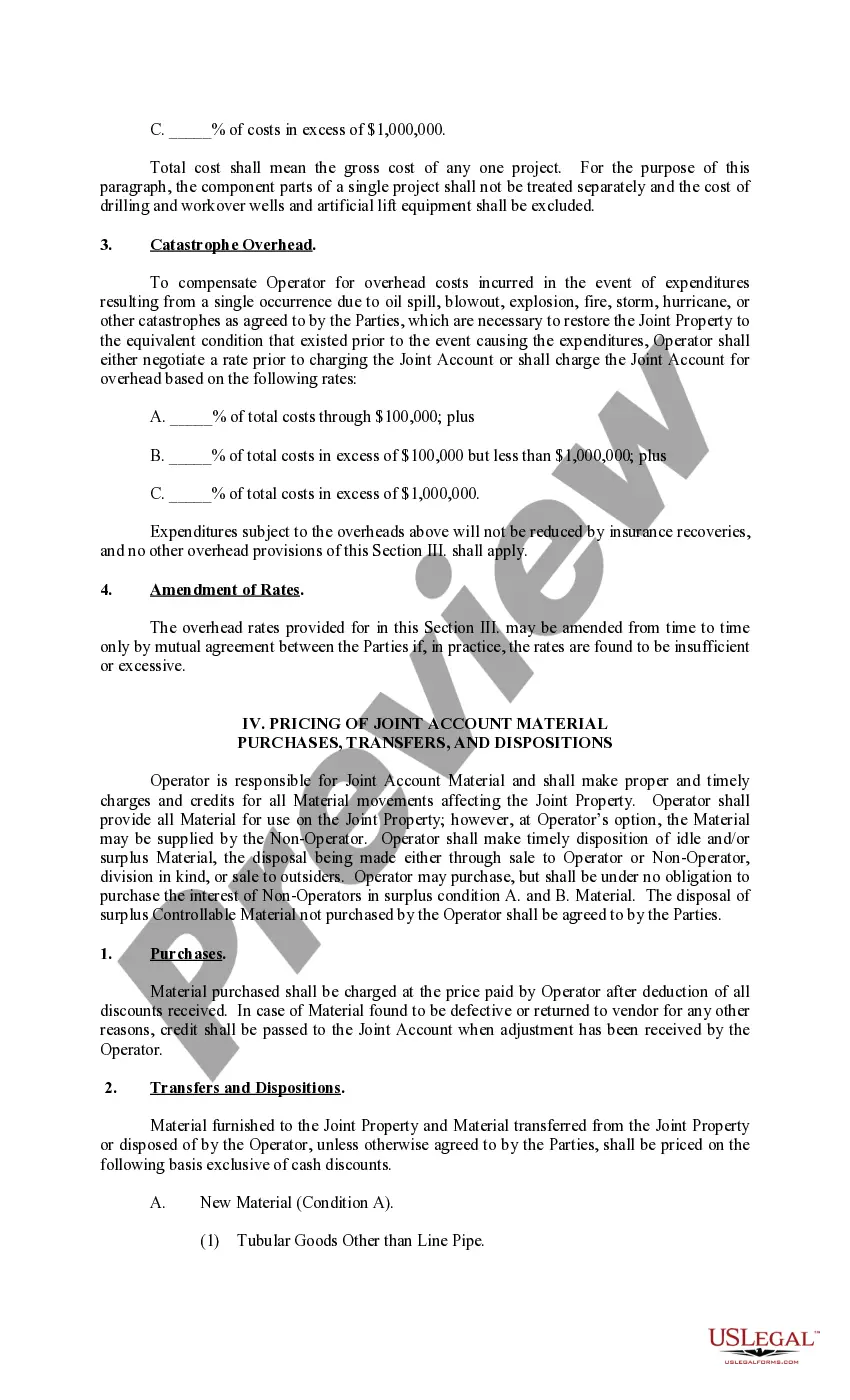

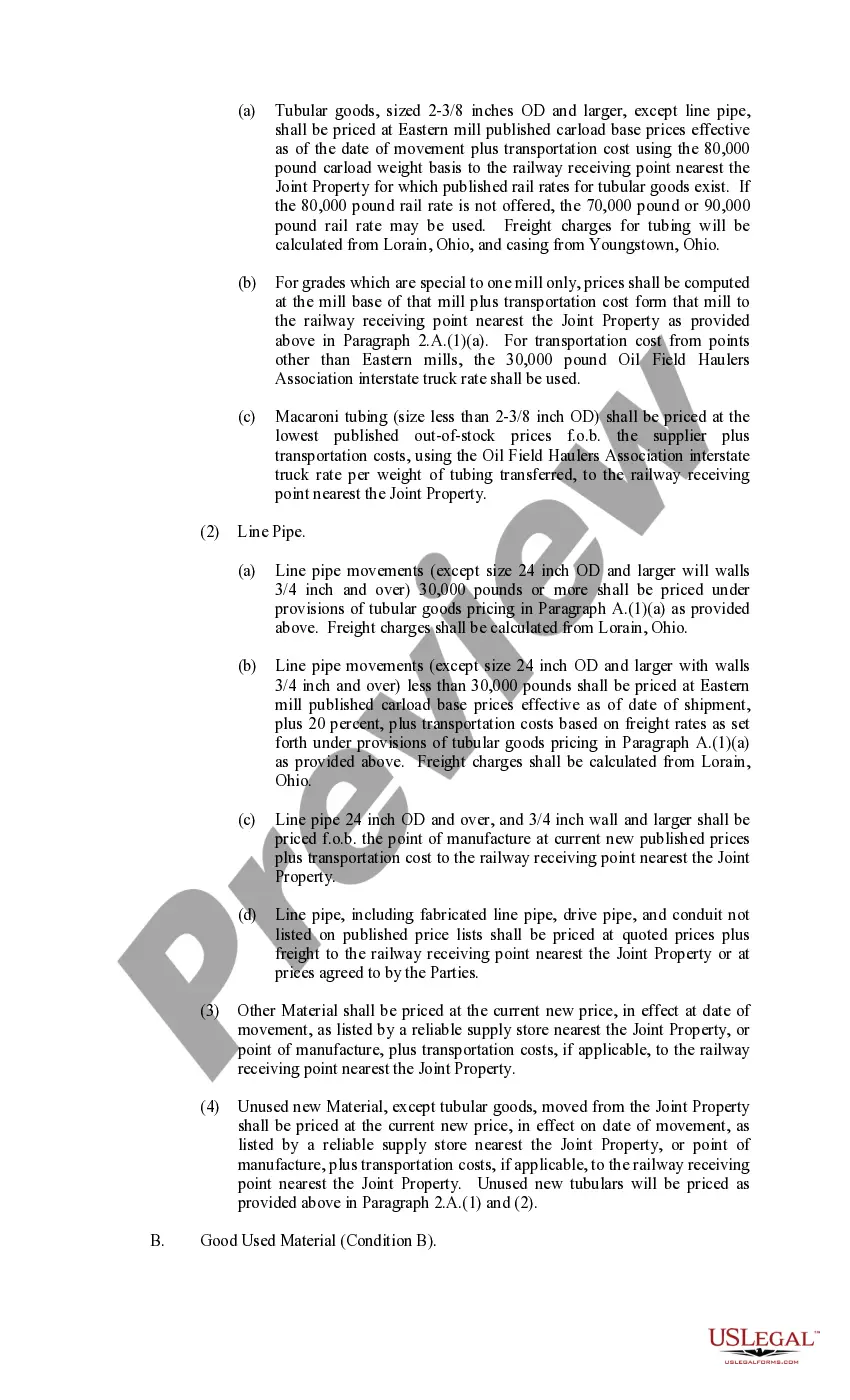

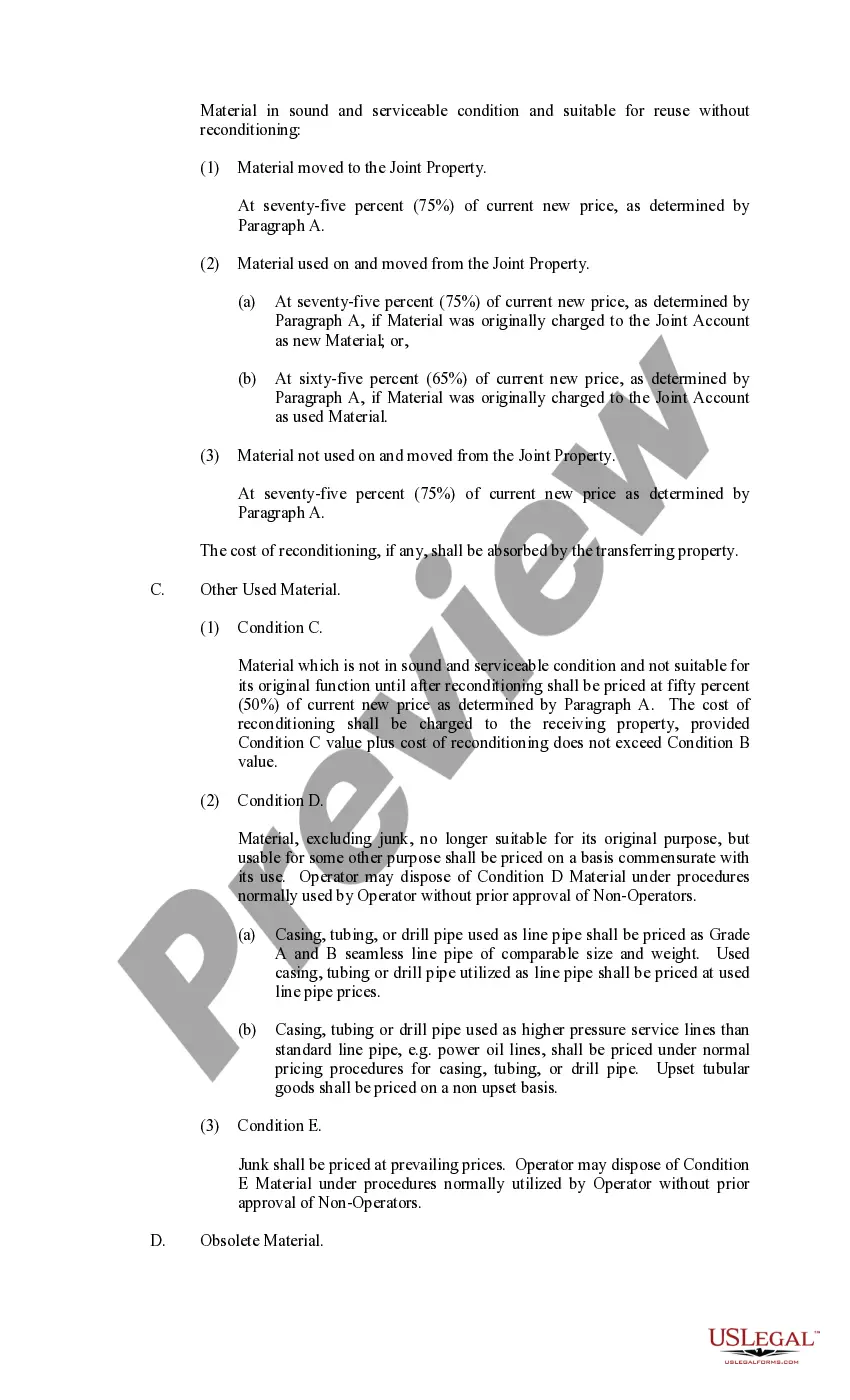

Wake North Carolina Exhibit C Accounting Procedure Joint Operations refers to the accounting procedures followed in joint operations conducted in Wake County, North Carolina. Joint operations are collaborative efforts between multiple entities or organizations to achieve a common goal. These accounting procedures ensure transparent and accurate financial reporting, recording, and analysis of joint operational activities. They provide a systematic framework for tracking expenses, revenues, assets, and liabilities incurred in joint operations. Keyword: Wake North Carolina Exhibit C Accounting Procedure Joint Operations Description: — Overview: Wake North Carolina Exhibit C Accounting Procedure Joint Operations guide and govern the financial aspects of joint operations conducted in Wake County, North Carolina. It ensures the proper allocation of expenses and revenues among participating entities. — Accounting Principles: These procedures adhere to generally accepted accounting principles (GAAP) to maintain consistency, accuracy, and transparency in financial reporting. They outline the specific guidelines for recognizing, measuring, and disclosing joint operational activities. — Financial Reporting: Wake North Carolina Exhibit C Accounting Procedure Joint Operations require timely and standardized financial reporting providing stakeholders with comprehensive information about the joint operations. This includes income statements, balance sheets, cash flow statements, and accompanying notes. — Expense Allocation: The procedures ensure fair and equitable allocation of expenses incurred during joint operations among the participating organizations. They provide detailed guidelines for cost allocation methods, such as proportional sharing based on ownership interests or activity-based costing. — Revenue Sharing: Wake North Carolina Exhibit C Accounting Procedure Joint Operations dictate the proper distribution of revenues generated through joint operations. They specify revenue recognition methods and guide the determination of each entity's share based on agreed-upon terms and conditions. — Asset and Liability Recording: These procedures outline the accounting treatment for joint operational assets and liabilities. They establish guidelines for recording and valuing assets contributed, acquired, or divested during the joint operations. Similarly, they ensure the appropriate recognition and measurement of liabilities incurred. — Auditing and Compliance: To ensure adherence to the accounting procedures and regulations, Wake North Carolina Exhibit C Accounting Procedure Joint Operations may require external audits or internal control assessments. These measures help maintain financial integrity and accountability. Types of Wake North Carolina Exhibit C Accounting Procedure Joint Operations (if applicable): — Public-Private PartnershipsPPPPs): This type of joint operation involves collaboration between governmental entities and private companies to deliver public services or infrastructure projects. Wake County may have specific accounting procedures for PPP. — Non-Profit Joint Ventures: When multiple non-profit organizations work together for a common purpose, Wake North Carolina Exhibit C Accounting Procedure Joint Operations can include specific guidelines for financial reporting and expense/revenue sharing in such joint ventures. — Academic Collaborations: Joint research projects or educational initiatives between academic institutions may require specific accounting procedures tailored to the unique financial aspects of these joint operations. Wake County may have relevant guidelines for such collaborations. In summary, Wake North Carolina Exhibit C Accounting Procedure Joint Operations are comprehensive guidelines that govern the financial aspects of joint operations in Wake County, North Carolina. These procedures facilitate transparency, accuracy, and compliance in financial reporting, expense allocation, revenue sharing, and asset/liability recording. Various types of joint operations, such as PPP, non-profit joint ventures, and academic collaborations, may have specific accounting procedures within the Wake County framework.

Wake North Carolina Exhibit C Accounting Procedure Joint Operations

Description

How to fill out Wake North Carolina Exhibit C Accounting Procedure Joint Operations?

Preparing legal documentation can be cumbersome. In addition, if you decide to ask an attorney to write a commercial agreement, papers for ownership transfer, pre-marital agreement, divorce papers, or the Wake Exhibit C Accounting Procedure Joint Operations, it may cost you a fortune. So what is the best way to save time and money and draft legitimate documents in total compliance with your state and local regulations? US Legal Forms is a perfect solution, whether you're searching for templates for your individual or business needs.

US Legal Forms is the most extensive online catalog of state-specific legal documents, providing users with the up-to-date and professionally verified templates for any use case collected all in one place. Therefore, if you need the latest version of the Wake Exhibit C Accounting Procedure Joint Operations, you can easily find it on our platform. Obtaining the papers requires a minimum of time. Those who already have an account should check their subscription to be valid, log in, and select the sample by clicking on the Download button. If you haven't subscribed yet, here's how you can get the Wake Exhibit C Accounting Procedure Joint Operations:

- Glance through the page and verify there is a sample for your area.

- Check the form description and use the Preview option, if available, to make sure it's the sample you need.

- Don't worry if the form doesn't satisfy your requirements - search for the correct one in the header.

- Click Buy Now when you find the required sample and select the best suitable subscription.

- Log in or register for an account to purchase your subscription.

- Make a payment with a credit card or via PayPal.

- Choose the document format for your Wake Exhibit C Accounting Procedure Joint Operations and save it.

Once finished, you can print it out and complete it on paper or upload the template to an online editor for a faster and more convenient fill-out. US Legal Forms enables you to use all the documents ever obtained many times - you can find your templates in the My Forms tab in your profile. Give it a try now!