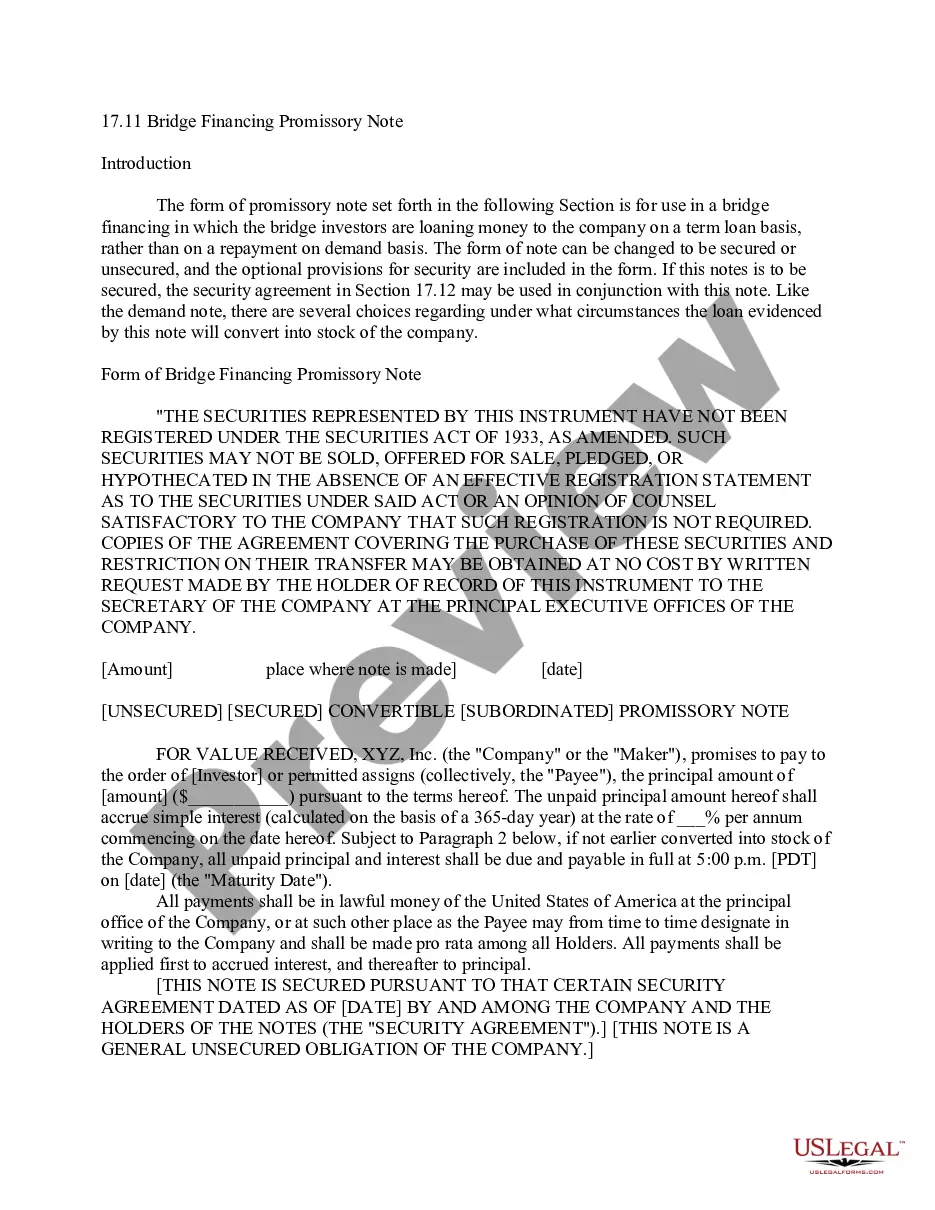

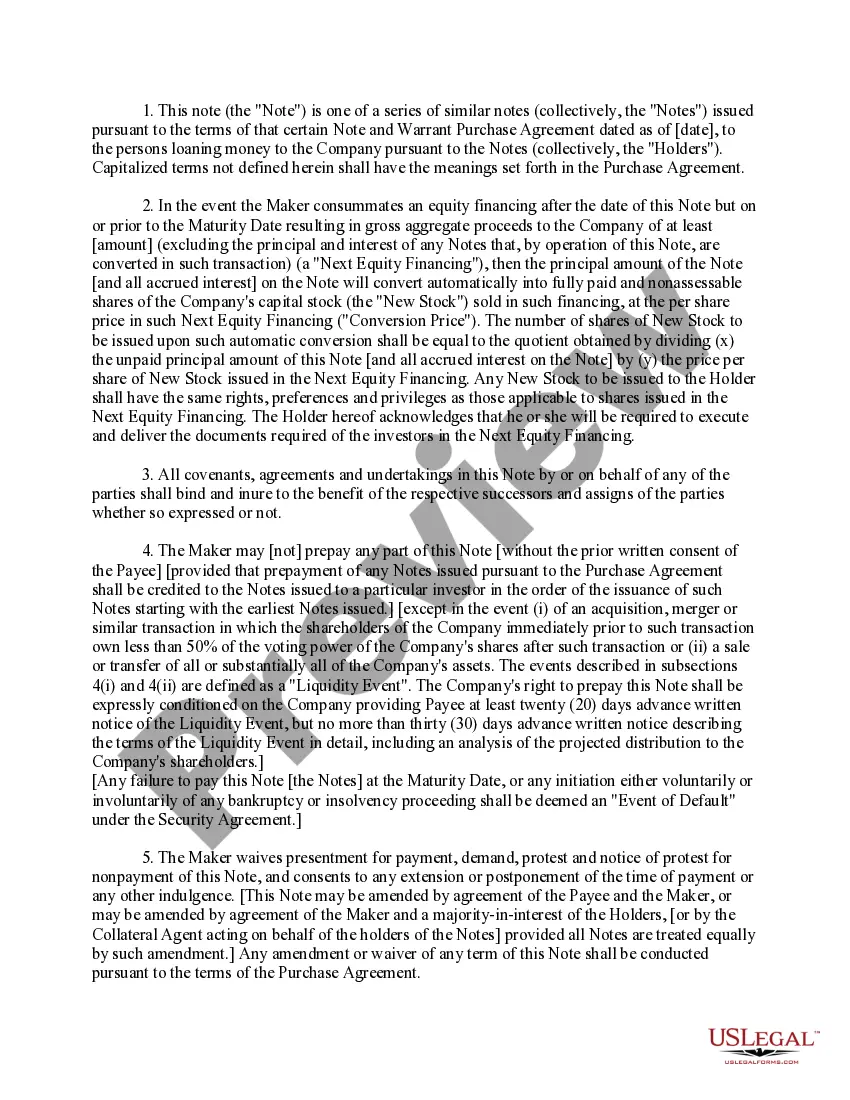

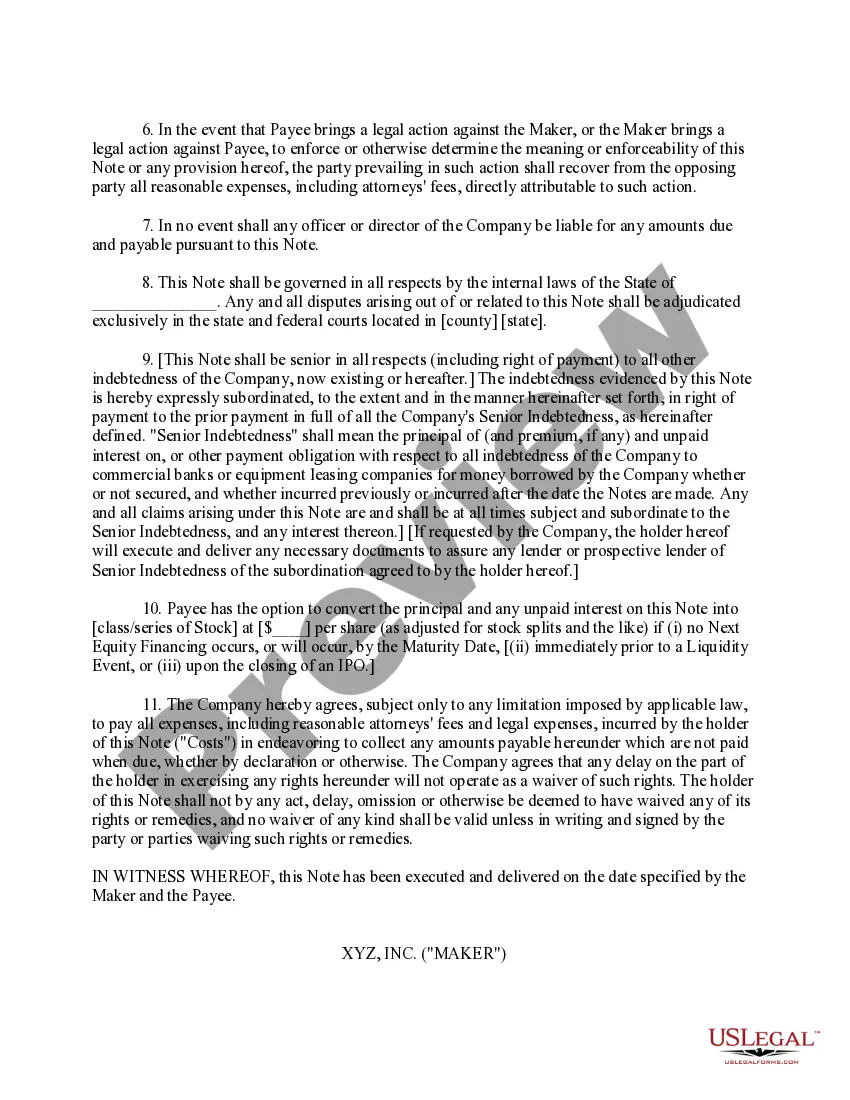

This document is for use in a bridge financing in whci the bridge investors are loaning money to the company on a loan basis, rather than on a repayment on demand basis. The form of the note can be changed to be secured or unsecured, and the optional provisions for security are included in the form.

Palm Beach Florida Bridge Financing Promissory Note is a legal document that outlines the terms and conditions of a short-term loan used for real estate transactions. This type of financing is often utilized when there is a gap between the sale of one property and the purchase of another. It acts as a temporary solution to bridge the financial gap until more permanent financing can be obtained. A Bridge Financing Promissory Note in Palm Beach Florida typically includes key details such as the loan amount, interest rate, repayment schedule, and any collateral that may be used to secure the loan. This document serves as evidence of the borrower's debt and their commitment to repay the loan according to the agreed-upon terms. There are different types of Palm Beach Florida Bridge Financing Promissory Notes that can be customized to meet the unique needs of each borrower. These include: 1. Straight Bridge Loan: This is the most common type of bridge financing where the borrower uses the loan to bridge the gap between the sale of their current property and the purchase of a new one. 2. Renovation Bridge Loan: This type of promissory note is used when the borrower needs short-term financing to renovate or upgrade a property before selling it. 3. Non-Recourse Bridge Loan: In this case, the borrower is not personally liable for the repayment of the loan. If they default, the lender can only take possession of the collateral, typically the property being financed. 4. Bridge-to-Construction Loan: This form of financing is commonly used when a property owner needs funding to start construction or development before obtaining long-term financing. Regardless of the type of Palm Beach Florida Bridge Financing Promissory Note, it's important for borrowers to carefully review the terms and consult with a qualified professional, such as an attorney or financial advisor. This will ensure that they fully understand their obligations and the potential risks associated with the loan.Palm Beach Florida Bridge Financing Promissory Note is a legal document that outlines the terms and conditions of a short-term loan used for real estate transactions. This type of financing is often utilized when there is a gap between the sale of one property and the purchase of another. It acts as a temporary solution to bridge the financial gap until more permanent financing can be obtained. A Bridge Financing Promissory Note in Palm Beach Florida typically includes key details such as the loan amount, interest rate, repayment schedule, and any collateral that may be used to secure the loan. This document serves as evidence of the borrower's debt and their commitment to repay the loan according to the agreed-upon terms. There are different types of Palm Beach Florida Bridge Financing Promissory Notes that can be customized to meet the unique needs of each borrower. These include: 1. Straight Bridge Loan: This is the most common type of bridge financing where the borrower uses the loan to bridge the gap between the sale of their current property and the purchase of a new one. 2. Renovation Bridge Loan: This type of promissory note is used when the borrower needs short-term financing to renovate or upgrade a property before selling it. 3. Non-Recourse Bridge Loan: In this case, the borrower is not personally liable for the repayment of the loan. If they default, the lender can only take possession of the collateral, typically the property being financed. 4. Bridge-to-Construction Loan: This form of financing is commonly used when a property owner needs funding to start construction or development before obtaining long-term financing. Regardless of the type of Palm Beach Florida Bridge Financing Promissory Note, it's important for borrowers to carefully review the terms and consult with a qualified professional, such as an attorney or financial advisor. This will ensure that they fully understand their obligations and the potential risks associated with the loan.