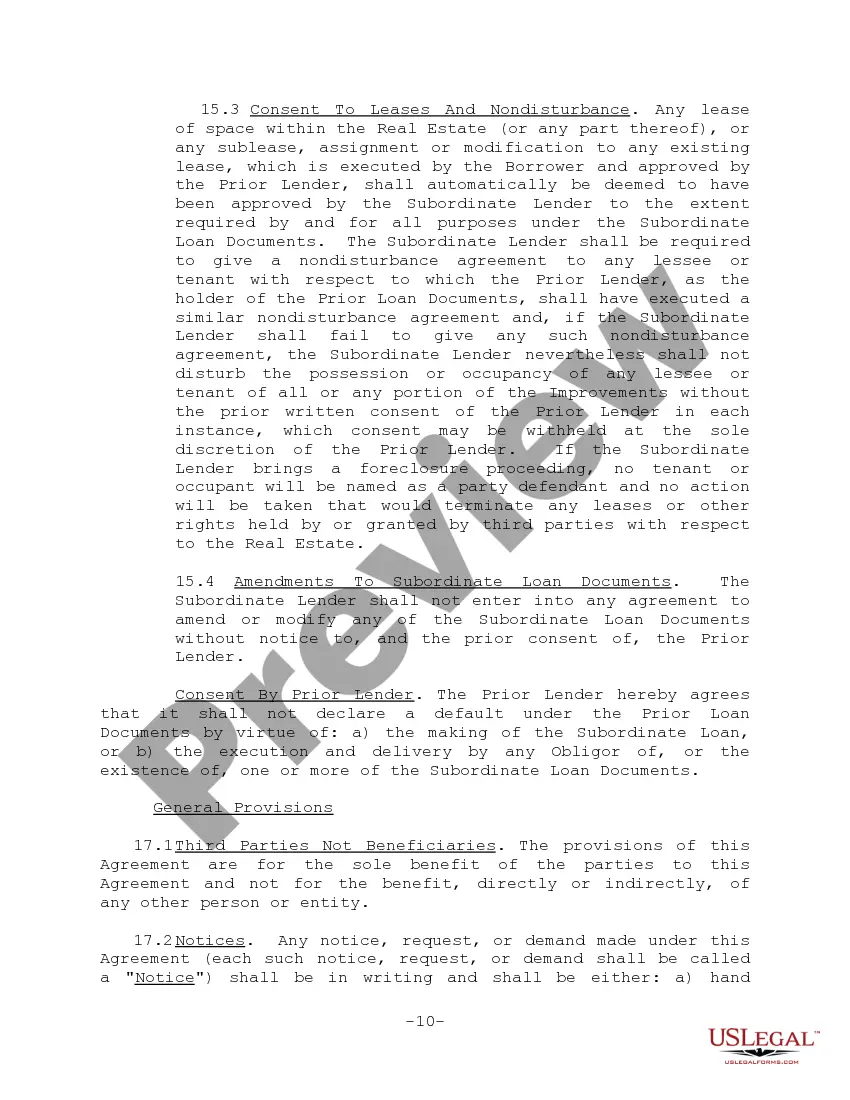

"Subordination Agreement Form and Variations" is a American Lawyer Media form. This is a subordination agreement with variations form.

A Wake North Carolina Subordination Agreement Form acts as a legally binding contract that establishes the priority of one party's rights over another party's claims on a particular property. This type of agreement occurs when a property owner wishes to obtain new financing or refinancing for their property while an existing mortgage or lien is already in place. The Wake North Carolina Subordination Agreement Form allows the property owner to obtain a new loan by consenting to a lower priority position for their new lender, which means that in the event of default or foreclosure, the existing lender will have the first claim or priority on the proceeds from the sale of the property. This agreement ensures that the new lender is aware of the current mortgage or lien and agrees to be in a secondary or subordinate position. There are several variations of the Wake North Carolina Subordination Agreement Form, depending on the specific circumstances and parties involved: 1. Mortgage Subordination Agreement: This type of agreement is used when a property owner wants to refinance their existing mortgage or obtain a second mortgage. The agreement ensures that the new mortgage is subordinate to the existing one. 2. Lien Subordination Agreement: This agreement is relevant when a property owner wishes to take out a loan or obtain financing while there is an existing lien on the property. The lien holder agrees to subordinate their claim or priority to the new lender. 3. Subordinate Financing Agreement: This form is applicable when a property owner seeks additional financing or lines of credit, making sure that the new lender's rights are subordinate to any existing mortgages or liens. Overall, a Wake North Carolina Subordination Agreement Form and its variations play a vital role in property transactions by establishing the priority of different creditors or lenders. Property owners and lenders alike utilize this form to protect their interests and define their rights in case of default or foreclosure.A Wake North Carolina Subordination Agreement Form acts as a legally binding contract that establishes the priority of one party's rights over another party's claims on a particular property. This type of agreement occurs when a property owner wishes to obtain new financing or refinancing for their property while an existing mortgage or lien is already in place. The Wake North Carolina Subordination Agreement Form allows the property owner to obtain a new loan by consenting to a lower priority position for their new lender, which means that in the event of default or foreclosure, the existing lender will have the first claim or priority on the proceeds from the sale of the property. This agreement ensures that the new lender is aware of the current mortgage or lien and agrees to be in a secondary or subordinate position. There are several variations of the Wake North Carolina Subordination Agreement Form, depending on the specific circumstances and parties involved: 1. Mortgage Subordination Agreement: This type of agreement is used when a property owner wants to refinance their existing mortgage or obtain a second mortgage. The agreement ensures that the new mortgage is subordinate to the existing one. 2. Lien Subordination Agreement: This agreement is relevant when a property owner wishes to take out a loan or obtain financing while there is an existing lien on the property. The lien holder agrees to subordinate their claim or priority to the new lender. 3. Subordinate Financing Agreement: This form is applicable when a property owner seeks additional financing or lines of credit, making sure that the new lender's rights are subordinate to any existing mortgages or liens. Overall, a Wake North Carolina Subordination Agreement Form and its variations play a vital role in property transactions by establishing the priority of different creditors or lenders. Property owners and lenders alike utilize this form to protect their interests and define their rights in case of default or foreclosure.